How to cut down Organizational cost -3

How to cut down

Organizational cost -3

Organizational cost -3

– A Case Study-

( Written by N.R. Jayaraman )

The following was another proposal given.

Overlapping working during lunch hour / merging

two shifts or increasing productivity

with more pay wherever possible

On one of the machines three men produced eight brackets in one shift . The lunch hour was half an hour in between both the halves of the shift. Due to the lunch break, the machine had to be stopped ten minutes before lunch and actual production commenced after 10 minutes after lunch because the machines had to be stopped and re started. The same is the case in the morning before commencing the work and machine had to stop before ten minutes at the closing of the shift. In view of the said action, the production also do not commence immediately and takes few more minutes. Thus around 45 to 50 minutes was actually lost in eight hour shift besides the lunch break.

Each worker was paid 200 per head and the wages per shift worked out to 3 x 200 = 600.

In the restructure scheme it was suggested to continue the work without stopping the machine during the lunch hour by giving staggering lunch for each worker. One of the three worker will go to lunch half an hour before actual lunch commenced, the second person will go in actual lunch break, and the third person will go at the end of the lunch. With the nonstop working of the machine during the lunch hour the production went up by three more brackets. Thus instead of eight brackets, eleven brackets could be manufactured. In order to encourage the workers to do the same, they were paid 1.5 hours extra wages per shift i.e. 20% increase in the per shift wage, for the staggering lunch even though they enjoyed 30 minutes lunch break individually.

Both the scenario resulted in the cost of the bracket and subsequent profit margin as below:

Production in Normal working : 8 Brackets

No of workmen engaged : 3 Nos

Wages paid : @ 200 each totaling to 3 x 200 = 600

Material and other cost including overheads per bracket = 500

Wages worked out per bracket : 600 ÷ 8 = 75

Sale price of bracket : 1000

Margin of profit : 1000- 575 (500+75) = 425 per bracket

Margin of profit per shift in Normal working :

(1000 x 8 = 8000) – (575 x8 =4600) = 3400

With Lunch hour working : 11 Brackets

No of workmen : 3 Nos ( Same as before)

Wages paid : @ 240 each ( 20% increase in wages) totaling to 3 x 240 = 720

Material and other cost including overheads per bracket = 500 ( Same as before)

Wages worked out per bracket: 720 ÷ 11 = 65.45

Sale price of bracket : 1000 ( Same as before)

Margin of profit : 1000- 565.45 (500+65.45) = 434.55 per bracket

Margin of profit per shift in Normal working :

(1000 x 11 = 11000) – (565.45 x 11 =66219.95 ) = 4780.05 i.e Rounded to 4780

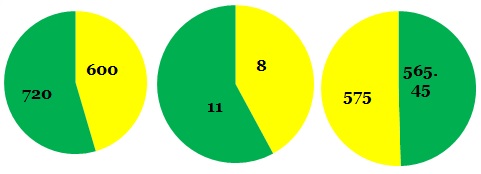

Wages for three Per day Per bracket

personnel production production cost

Margin of Profit per shift

If you see the graphic representation you can see that even with increase in wages to the workmen, the cost of production per bracket has come down because the production has gone up per shift due to the staggering lunch hour working. In the same manner the profit margin has also considerably increased. The yellow shades project the Normal working data and the Green represents the Staggered lunch data.

…….continued

Recent Comments